Its the age old debate on which generation had it tougher, thrown in the spotlight with the current economic backdrop and so, as we delve deeper into the issue of buyer affordability over the years, it becomes evident that the house buying landscape has undergone significant transformations, placing increasing challenges on prospective homebuyers.

The financial burden on first-time buyers has escalated, largely due to the substantial disparity between income growth and skyrocketing property prices, alongside recent mortgage rate hikes.

Comparing the current generation of first-time buyers with that of previous decades, the discrepancy is startling.

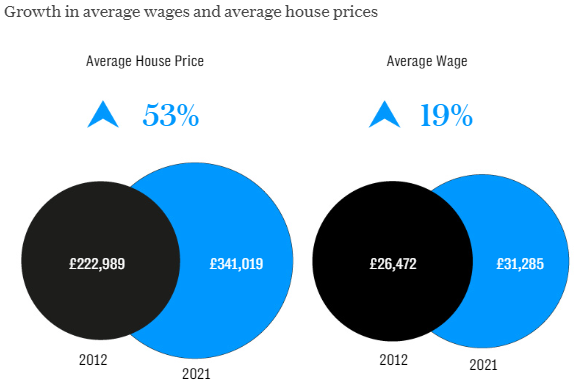

Wages have only risen by 19% while property prices have surged by 53% between 2012 and 2021, leading to a staggering 179% increase in property prices compared to income growth during this period. Consequently, aspiring homeowners are finding it increasingly difficult to enter the property market at a young age. The average age of first-time buyers has risen over the years as they struggle to keep pace with slow wage growth, rising rental costs, and exorbitant property prices.

One of the most significant indicators of this affordability crisis is the percentage of mortgage payments as a proportion of income. Currently, this figure stands at its highest point in 15 years, exceeding the long-run average of 30%.

One of the most significant indicators of this affordability crisis is the percentage of mortgage payments as a proportion of income. Currently, this figure stands at its highest point in 15 years, exceeding the long-run average of 30%.

However, it is important to note that despite the current challenges, this ratio is still lower than the peak experienced in the late 1980s. The average first-time buyer now has, or needs, a deposit in excess of £60,000, and this has doubled over the past 15 years. In response to these challenging circumstances, the "Bank of Mum and Dad" has become an invaluable source of support for many first-time buyers.

With higher deposit requirements, parents and family members are stepping in to assist their children in purchasing their first homes, marking a significant increase in support compared to a decade ago.

To adapt to the rising need for larger deposits and the strain on affordability, buyers are resorting to longer-term mortgages as well. Approximately 38% of all mortgage applicants are now choosing 30-35 year mortgage terms, and an astonishing 67% of mortgages available on the market offer terms up to 40 years.

While this eases the immediate burden of monthly payments, it is crucial to recognize that longer-term mortgages result in significantly higher interest payments over time. For instance, a 6% mortgage on a £250,000 property over 40 years could accumulate £206,000 in interest, compared to £80,000 less over the same mortgage paid off in 25 years.

This highlights the importance of carefully considering the long-term financial implications of opting for extended mortgage terms. The financial strain is not restricted to specific regions; it is a nationwide issue.

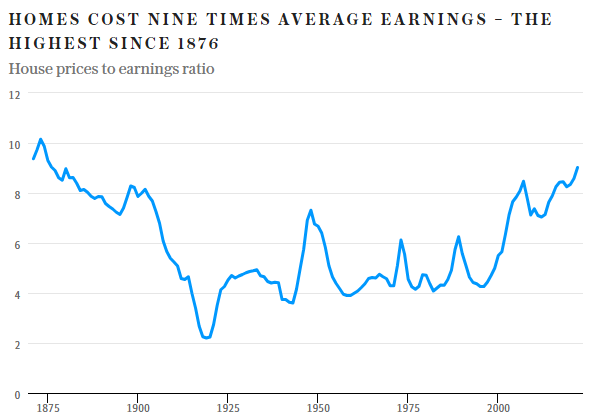

House prices are now at a startling 9 times the average earnings, marking the highest ratio since 1876.

House prices are now at a startling 9 times the average earnings, marking the highest ratio since 1876.

The Birmingham area, in particular, currently faces a ratio of 6.3, indicating a concerning trend of stretched affordability across the country.

As we look to the future, it is essential for policymakers and industry stakeholders to address the growing issue of buyer affordability.

A lack of property being built is another factor, as there is currently a backlog of 4.3 million homes. The government target building 300,000 homes per year but this has not been achieved since 1969.

Tacking this problem would mean either building 442,000 homes per year over the next 25 years or 654,000 per year over the next decade in England alone.

Amidst these complex economic dynamics, the pursuit of homeownership endures as an enduring aspiration, it has for each generation, so I will let you continue with the family get together debates with some stats in your back pocket.

For further discussions on this analysis, feel free to reach out to me for further information that may help you in your home move.

Andy McHugo

0121 5170251 andy@mchugohomes.co.uk

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link