The start of 2025 has been intriguing for local property market in Harborne and Edgbaston. Here’s a concise, bullet-point overview of the key statistics and trends from January:

Market Activity & Pricing

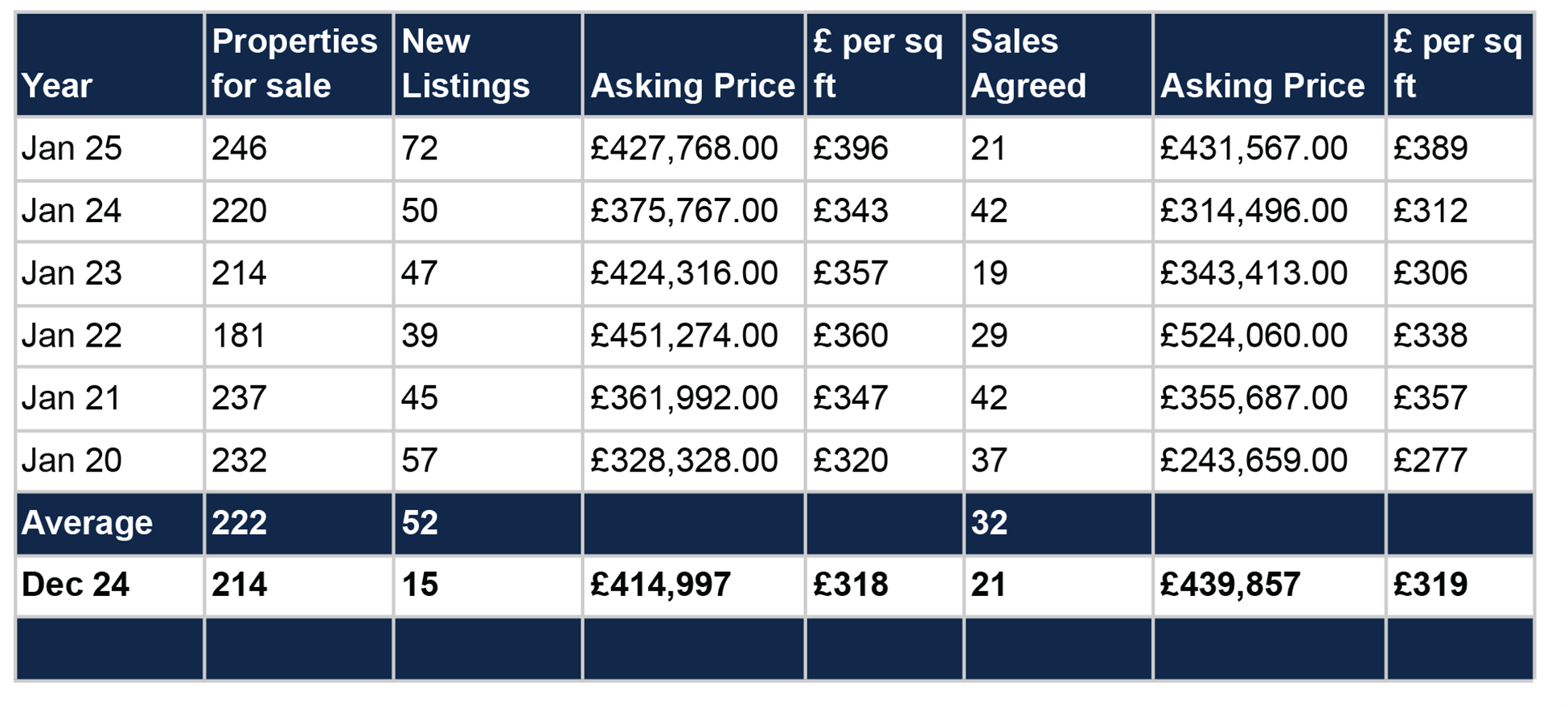

B17 Segment Highlights:

- Properties for Sale: Average of 222 listings (e.g. Jan 25: 246, Jan 24: 220).

- New Listings: Average of 52 new listings per month.

- Asking Prices:

- New listings average around £427,768 with approximately £396 per sq ft.

- Agreed sale prices average about £431,567 with roughly £389 per sq ft.

- Price Trends:

- New listing asking prices increased by 1.75% compared to last year.

- Agreed sale prices saw a 3.44% rise year-on-year.

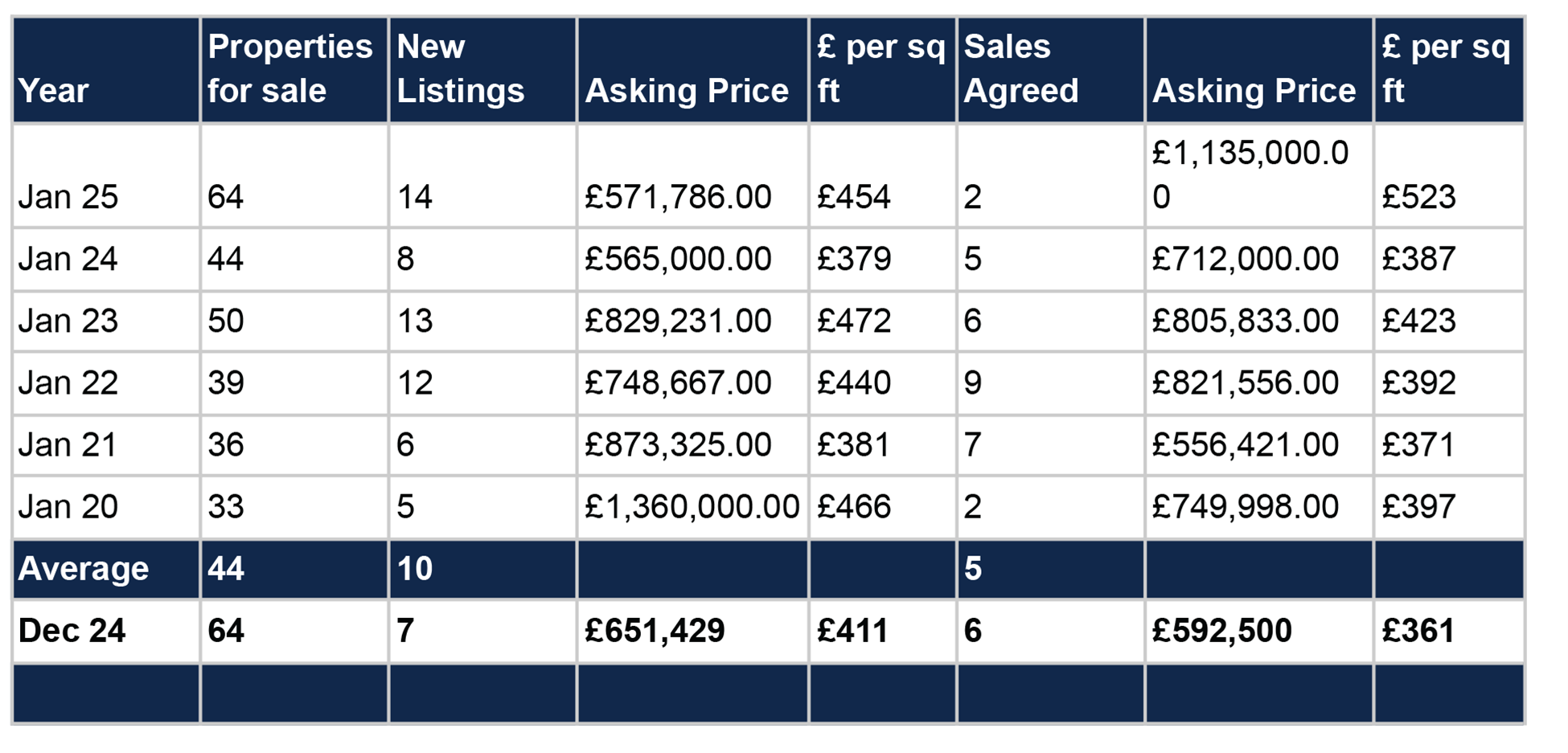

B15 Segment Highlights:

- Properties for Sale: Average of 44 listings (e.g. Jan 25: 64 listings, although smaller scale compared to B17).

- New Listings: Average of 10 new listings.

- Pricing:

- New listings show higher values, averaging around £571,786 with about £454 per sq ft.

- Agreed sales in this segment have higher per square foot prices, averaging £523 per sq ft.

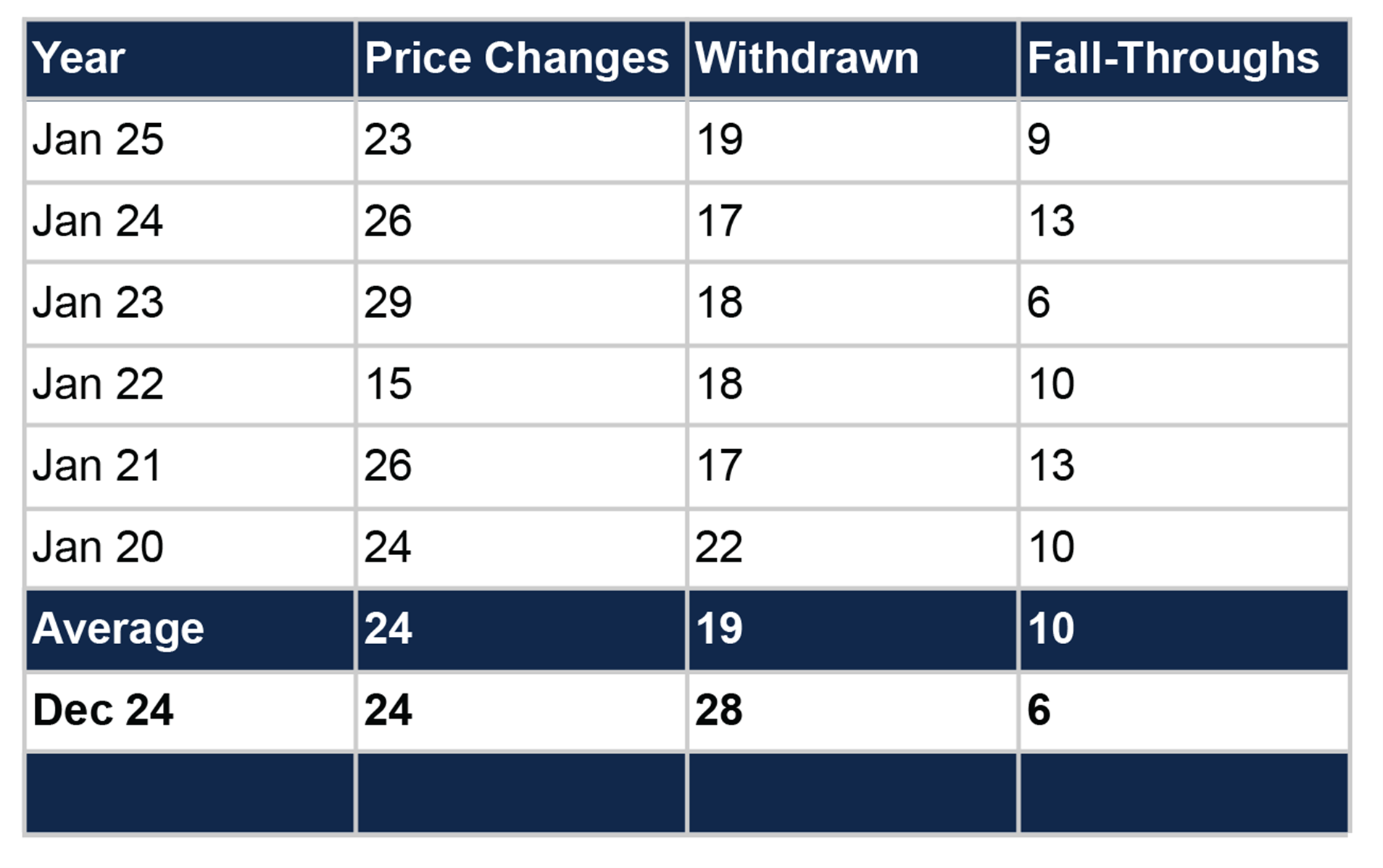

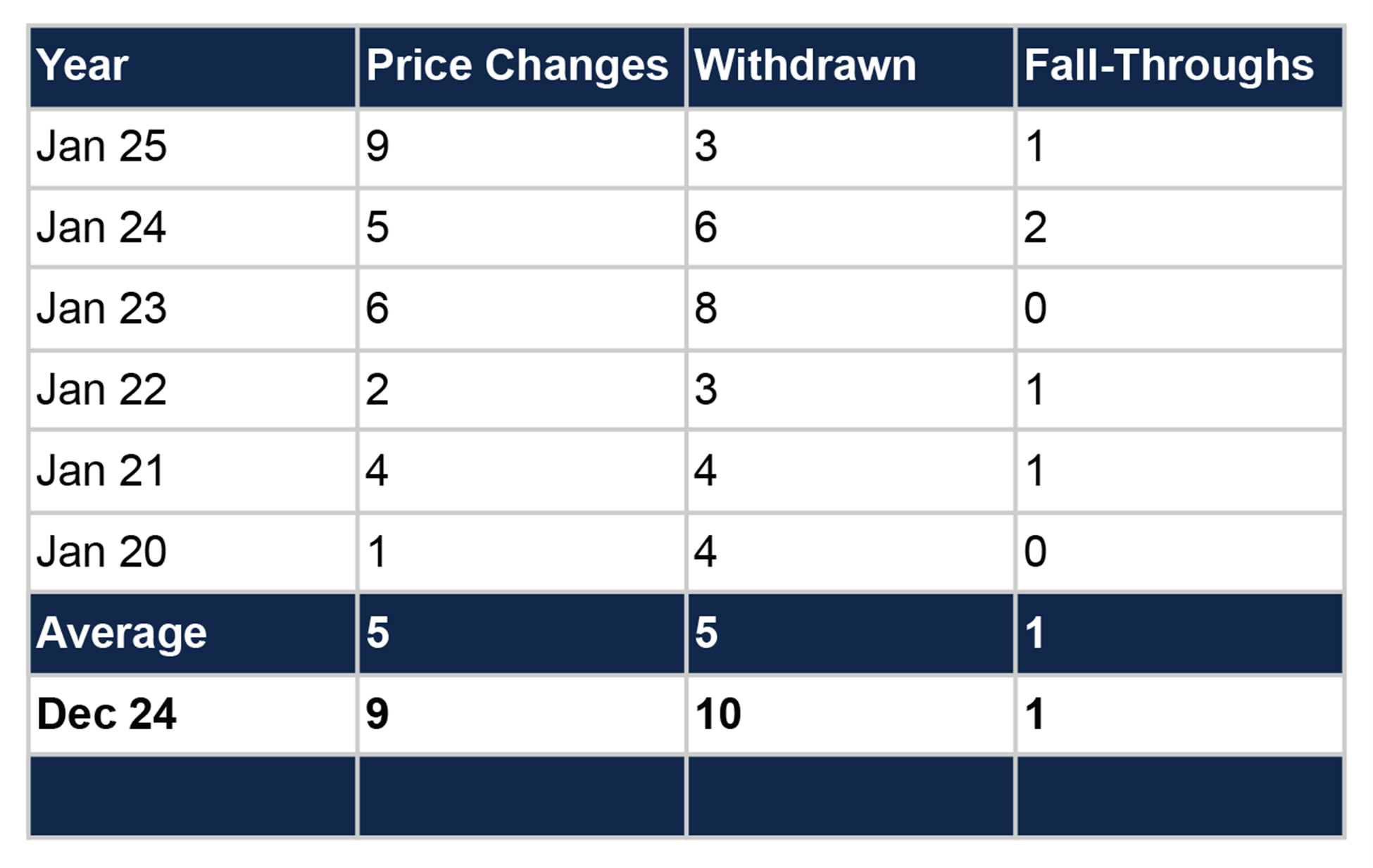

- Price Adjustments: Fewer price reductions compared to previous years suggest sellers are pricing more realistically from the outset.

Overall Market Trends:

- Increased property activity relative to both last January and the six-year average.

- A reduced number of properties are being withdrawn from the market, signalling more committed sellers.

- Despite some price adjustments still exceeding the six-year average, buyer confidence remains strong.

National Economic & Mortgage Environment

Inflation & Mortgage Approvals:

- Inflation: Dropped to 2.5% in December; annual average for 2024 now stands at 2.53%.

- Mortgage Approvals:

- December saw a 1.22% increase on November and a significant jump compared to December 2023.

- The ‘effective’ interest rate on new mortgages is at its lowest since April 2023 (4.47%).

Lender Activity & Base Rate Adjustments:

- Mortgage Rate Cuts:

- Lenders such as Barclays, Coventry Building Society, and Halifax have reduced rates to stay competitive.

- New products and rate cuts (up to 0.3% on remortgage deals) are contributing to increased buyer activity.

Bank of England:

- The base rate was reduced by 25bps to 4.5% in February 2025.

- This cut is the lowest since June 2023 and has bolstered market sentiment, although fixed-rate mortgages remain largely unaffected due to pre-pricing.

House Price Index Insights:

- Monthly price increase of 0.25% and an annual rise of 2.06% indicate steady growth.

- Rightmove reported an 11% increase in new property listings and the largest price jump at the start of the year since 2020.

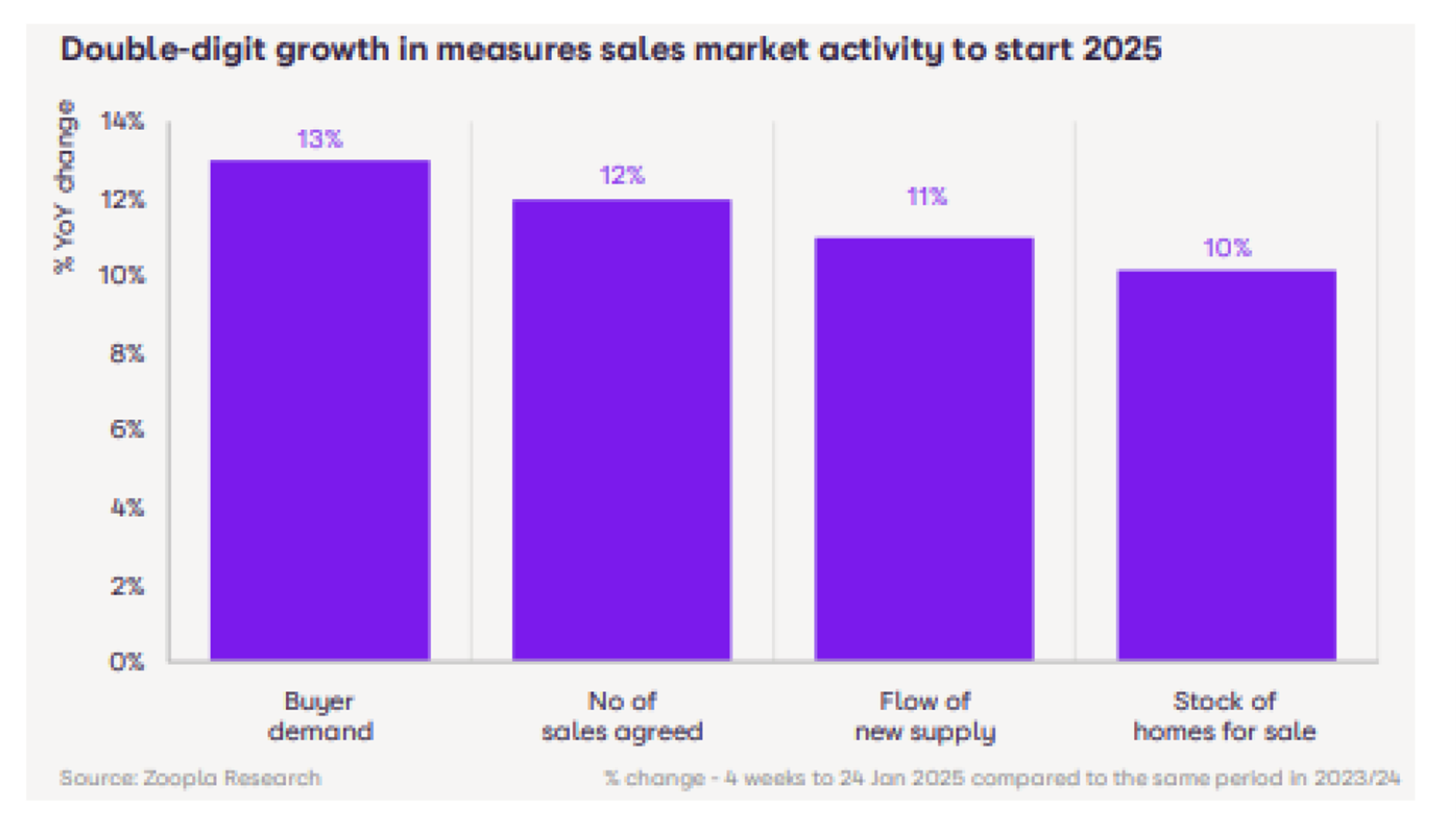

- Zoopla data confirms higher buyer demand and increased market activity.

Conclusion

Overall Outlook:

- January 2025’s data signals a resilient market with healthy activity levels and positive pricing trends.

- Despite ongoing affordability challenges, both buyers and sellers appear to be adapting well to the current economic climate.

- The combination of lower inflation, competitive mortgage rates, and supportive lender actions contribute to a cautiously optimistic forecast for the rest of the year.

- The local and UK property market is set for continued momentum in 2025.

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link